U.S. banks borrowed so heavily from the Federal Reserve and other liquidity providers during the recent crisis that the inflows outpaced the decline in deposits they were seeking to offset, according to new research from the Federal Reserve Bank of New York.

In early March, before depositors began withdrawing funds at an accelerated pace, banks replaced about 37% of their deposit runoff with outside borrowing. That share increased to 127% by late March, the research found.

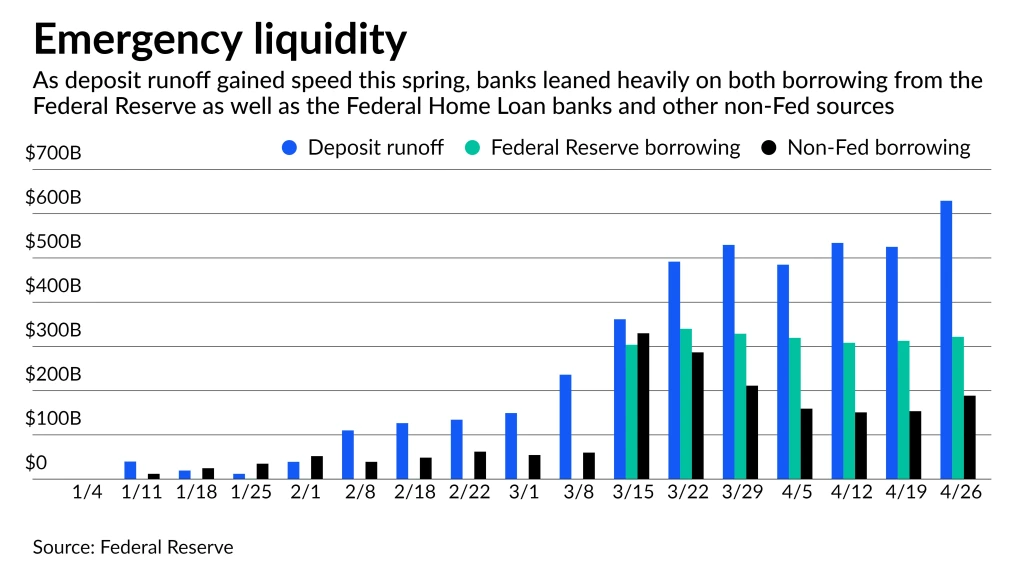

The New York Fed study quantifies the scramble for liquidity in March and April, when banks turned to the Federal Reserve and the Federal Home Loan Bank System to supplement fast-falling deposit balances.

Banks of all sizes — but especially those with between $50 billion and $250 billion of assets — acted with urgency after multiple failures shook the industry in March.

Borrowing in such large quantities suggests “significant and widespread demand for precautionary liquidity,” New York Fed researchers wrote in their analysis published earlier this month.

Financial institutions padded their liquidity with a mix of funds from the Fed, the Federal Home Loan banks and other private sources. The Fed offered banks funds via the discount window and the Bank Term Funding Program, a facility that the central bank opened in March to provide cash to banks concerned they might not be able to meet the requests of all depositors.

The spike in borrowing from the Fed and other sources followed a year when banks let deposits fall off their balance sheets without replacing them. Banks typically pay higher interest rates to borrow from sources outside their deposit base, where they have borrowed for next to nothing in recent years.

“It’s a lot more expensive than deposits, but the stability piece is important,” said Adam Stockton, director of retail deposits at Curinos, a financial services consulting firm.

Banks with between $50 billion and $250 billion of assets did the most borrowing from the FHLBs, other non-Fed sources and the Fed itself during and after the recent crisis, when some of their peers experienced significant deposit outflows.

Those banks borrowed an additional $381 billion in mid-March. Banks in other asset categories — both smaller and larger — borrowed considerably less over the same period.

The three banks that have failed since March — Silicon Valley Bank, Signature Bank and First Republic Bank — all had between $110 billion and $215 billion of assets at the end of 2022.

It wasn’t that long ago that banks found themselves with more deposits than they could put to use. For much of 2020 and 2021, banks of all sizes reported mountains of deposits, a side effect of the stimulus programs designed to keep consumers and businesses afloat during the COVID-19 pandemic.

But even before the crisis that started in March, banks were watching their deposits drop and competing with their peers for customers. When the Fed began to raise interest rates in March 2022, and continued to hike past industry expectations, bank customers parked their funds in higher-yielding spots, from money market funds to Treasury.

In recent weeks, banks have resumed borrowing less than they are losing in deposits. Total borrowing from the Fed and FHLBs totaled $510 billion at the end of April, below the estimated $630 billion in deposit runoff in the same period. But the most recent borrowing levels are still quite elevated for the industry, which borrowed less than $100 billion from the Fed and FHLBs in any given week before the crisis.

The industrywide decline in deposits means institutions are likely to struggle with falling net interest margins in the coming quarters, when they will have to pay higher rates to keep depositors, said Greg Feldberg, director of research at Yale University’s Program on Financial Stability.

The banking industry’s net interest margin fell slightly in the first quarter, which mostly preceded the banking crisis, according to a Barclays Research review of regulatory filings. Bank executives have said they expect net interest margin to decline further during the remainder of the year, thanks in part to higher deposit costs.

“There’s going to be a net interest margin issue for a while,” Feldberg said.